Using electronic payments for exponential business growth

Payments - 8 Sep 2017

Written by Christian van Stom

In today’s highly disrupted marketplace, competitive advantage has never been more important. The businesses that succeed share one thing in common: the ability to generate exponential return on investment. In a word leverage.

What is “payments”?

The “payments system” refers to a structure that enables consumers, businesses and organisations to transfer funds from an account at a financial institution (like a bank for example) to one another. The payments system includes “payment instruments”: cash, cheques and electronic funds transfers – the mediums used by customers to make payments. This also includes unseen arrangements that ensure funds move from accounts at one financial institution to another. “Electronic payments” include Credit and Debit Cards, BPAY, Internet and Phone Banking as opposed to “paper-based methods” such as Cash and Cheque.

Growth Levers

First let’s look at what leverage actually is. Described by Archimedes over 2,300 years ago levers underpin the growth of civilisation, everything from building the pyramids to the Sydney Harbour Bridge have been achieved through one of the most simple mechanisms ever invented. All that is required is a platform and a hinge and the lever is able to amplify input and create a significantly greater output. In modern times, the place where the real growth is delivered is online in real time. Marketing is about growth. Specifically, revenue growth. The companies that are winning have embraced payments as the newest growth platform, capable of delivering transactions at a greater speed than ever before. For example, the University of Sydney has recently announced that it has developed a new Blockchain-based system that can perform more than 440,000 transactions per second. (Australian FinTech)

Marketing is the process of creating customers which in turn results in revenue. Online payments is a growth lever utilised by marketers that generates growth in the following way:

Step 1: Creation: increase the number of customers

Step 2: Retention and growth: increase the value of transactions per customer

Step 3: Optimisation: reduce the cost per transaction

How electronic payments delivers growth

As we have seen even prior to the turn of the millennium, but growing sharply in the past 10 years, non-cash payments is growing significantly.

As mentioned earlier, the first part of leverage comes from the creation of a platform. As defined above, with relation to online payments, that platform consists of the most popular payment methods in use by customers today – Credit, Debit, BPAY and Internet and Phone Banking. This platform will continue to grow not only in size but also in breadth of options with contactless and mobile payments being the next frontier.

Step 1: Creation: increase the number of customers

The development of the platform leads to the first step for growth leverage: increase the number of customers.

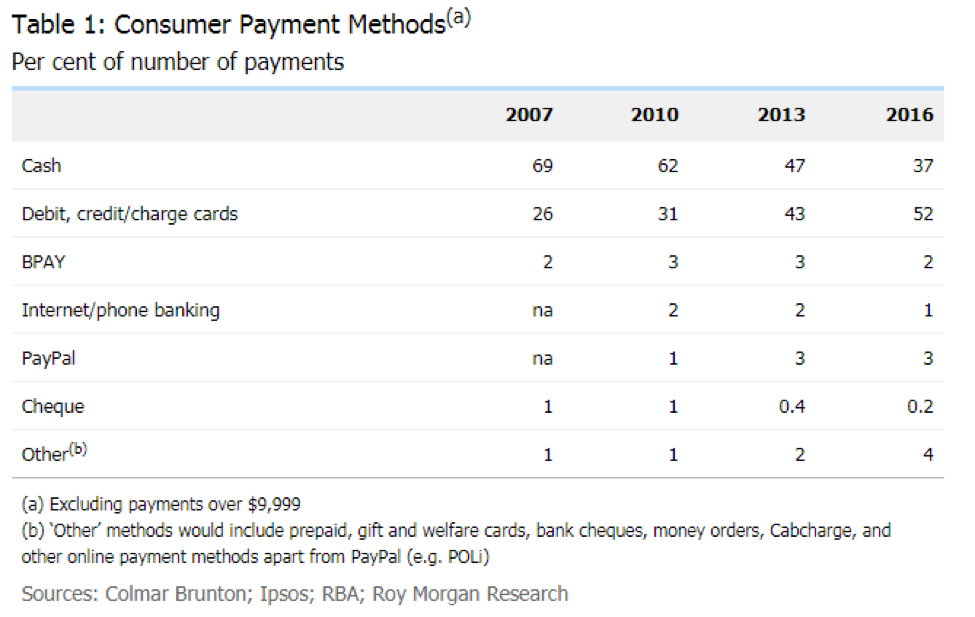

A survey completed by the RBA in 2016 demonstrated “Australian consumers are continuing to switch to electronic payment methods in preference to paper-based methods – cash and cheques – for their transactions. Credit and debit cards combined were the most frequently used means of payment in the 2016 survey, overtaking cash (Table 1).”

Step 2. Retention and growth: increase the value of transactions per customer

The continued decline in the transactional use of cash has been driven largely by the rise in the share of card payments. “Between 2013 and 2016, the share of payments (by number) made using credit and debit cards increased by 9 percentage points to 52 per cent.”(RBA)

One of the biggest challenges for businesses is increasing the bottomline. This brings us to the hinge in the payments growth lever. There are two main ways to increase output from customers once there is an established relationship. The first is to increase the value of the transactions and the second is to increase the frequency of the transactions per customer.

CBA notes that growth in value of transactions has increased 14% for online transactions since 2015 with the median purchase price of an online transaction up to 42% (2015-2016) from 37% (2014-2015). (CBA)

Step 3. Optimisation: reduce the cost per transaction

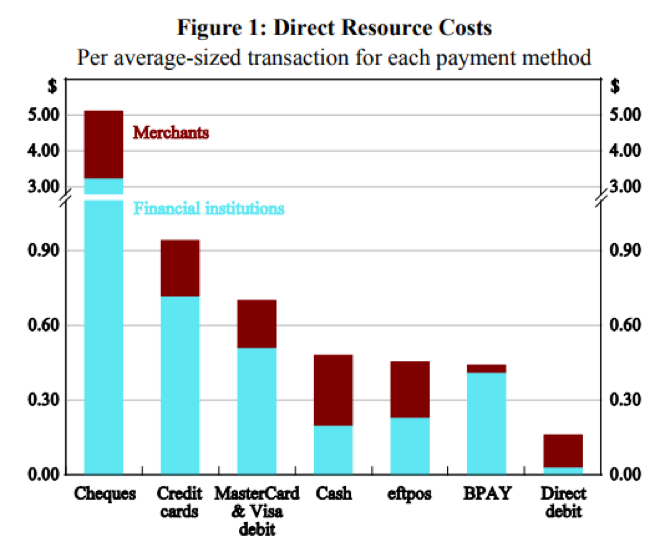

Finally, electronic payments delivers unbeatable cost savings when compared to the paper-based alternatives of cash and cheques. For example, a report by the RBA found that:

“Cash, eftpos and contactless MasterCard & Visa debit transactions have broadly similar resource costs for transactions of under $20. Above $20, eftpos is the lowest-cost payment method. At the average transaction size for each instrument, MasterCard & Visa debit card payments are 3 more resource intensive than eftpos, while credit card transactions are the most resource-intensive card payment method even when excluding the costs of credit and rewards. Of all methods considered in the study, direct debit remains the lowest cost, while cheques remain the most expensive.”

Reference: RBA

Summary

Due to the high growth and availability of customers, high value of transactions and a wide range of low cost payment methods, electronic payments is a key growth lever for Australian businesses. This is underpinned by a governing and regulatory body that is principled in providing a cost-effective and efficient payment system for businesses, consumers and the public sector, which has led to the high adoption rates for Credit Cards, Debit Cards, Eftpos, BPAY and Direct Debit.

Over time these advantages that electronic payments already provides will continue to be augmented with the broadening of the platform through contactless, mobile and in time the New Payments Platform.

When it comes to delivering increased return on investment, electronic payments is the key to creating, retaining and optimising business growth.

Subscribe to updates

Get the latest news and payment insights from Eway hot off the press.